Cybersecurity, antivirus, VPN, endpoint protection, and subscription-based SaaS companies sell legitimate security products, but payment processors often review them with more caution than ordinary software merchants. In 2026, stable processing depends on explaining the model clearly, reducing dispute risk before it becomes visible, and working with banking partners that understand recurring digital software.

Executive summary: Cybersecurity merchants are commonly reviewed for recurring billing practices, historical chargeback activity, affiliate marketing exposure, international sales, prior processor terminations, rolling reserve risk, and Visa VAMP exposure. The merchants that scale cleanly usually have transparent renewal communication, recognizable billing descriptors, dispute deflection tools, fraud controls, and strong documentation ready before underwriting asks for it.

Guide for Cybersecurity & Antivirus Companies

Cybersecurity and antivirus payment processing can feel complicated because several risk factors often overlap. This guide organizes the most important topics in one place so security software, VPN, SaaS, and subscription merchants can understand what processors review and how to prepare.

Cybersecurity Merchant Risk Mix

Illustrative underwriting mix based on the most common cybersecurity and antivirus merchant-account risk factors. Use it as a visual guide for what underwriters commonly review first.

Why Cybersecurity Merchants Face Extra Scrutiny

Security software is often sold online, delivered digitally, billed on a recurring basis, and marketed to customers across multiple countries. That combination can be profitable and scalable, but it also creates a risk profile underwriters want to understand before approving a merchant account.

A processor is not only asking whether the company is real. It is asking whether customers will recognize the charge, whether renewals are disclosed, whether cancellation is easy, whether affiliate traffic is controlled, whether chargebacks are trending upward, and whether the business can support the volume it wants to process.

The result is that antivirus and cybersecurity companies may encounter processor declines, rolling reserve requirements, volume caps, elevated underwriting review, and increased chargeback monitoring even when the product is legitimate.

Common Reasons Antivirus Companies Get Declined

- Recurring billing concerns: automatic renewals, trial-to-paid conversions, forgotten subscriptions, and unclear renewal terms can all increase dispute risk.

- Historical chargeback activity: even moderate dispute levels can trigger declines, reserves, or reduced monthly processing limits.

- Affiliate marketing exposure: underwriters may review ad claims, landing page disclosures, refund policies, and affiliate oversight controls.

- International processing activity: cross-border transactions can introduce fraud concerns, currency conversion issues, and geographic risk exposure.

- Prior processor terminations: reserve increases, account closures, and volume restrictions from a prior processor can follow a merchant into the next application.

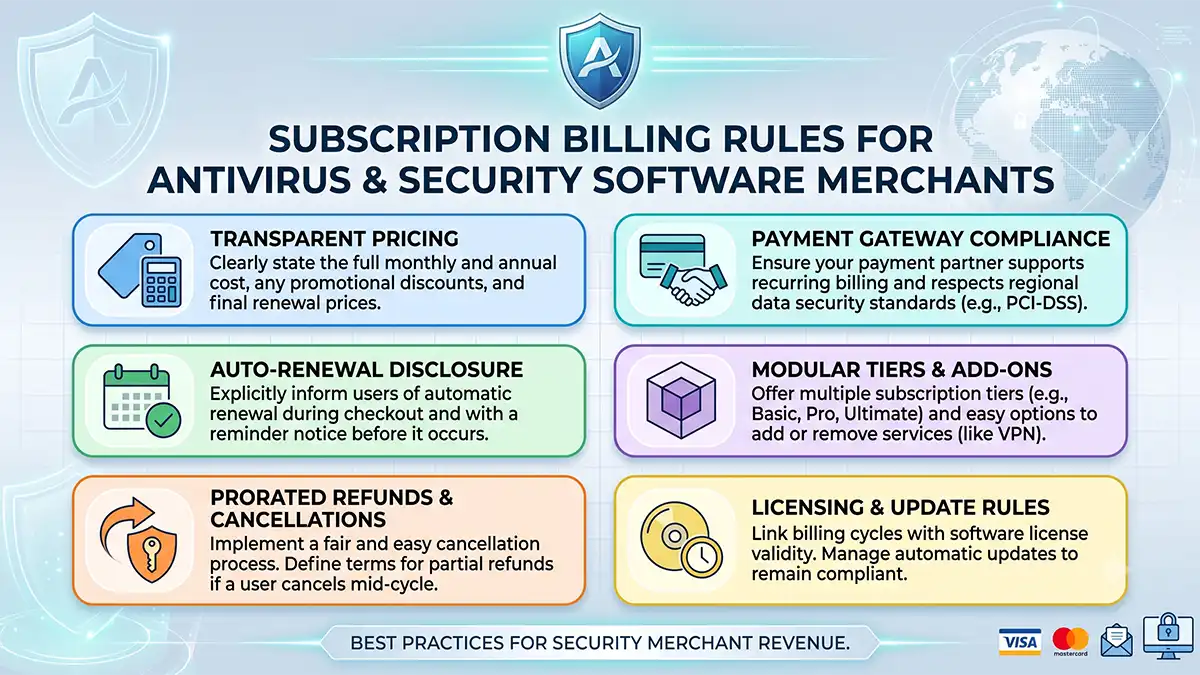

Subscription Billing Is the Center of the Risk Review

For antivirus and cybersecurity software, subscription billing is often the business model. The challenge is that recurring billing also creates the exact conditions that lead to friendly fraud: customers forget they enrolled, miss renewal notices, do not recognize the billing descriptor, or call the bank before contacting support.

A strong subscription program makes the terms obvious before purchase, repeats the renewal terms in confirmation messaging, sends advance renewal reminders, gives customers a direct cancellation path, and trains support teams to resolve refund questions quickly.

Underwriters increasingly want to see evidence of those controls. A clean checkout page, visible renewal terms, and a documented cancellation flow can materially improve the way a cybersecurity merchant account is viewed.

| Risk Area | What Processors Look For | What Merchants Should Prepare |

|---|---|---|

| Trial-to-paid billing | Clear consent and renewal timing | Checkout screenshots, terms, reminder emails |

| Billing descriptor | Recognizable company or product name | Descriptor examples and support phone visibility |

| Affiliate traffic | Truthful ads and landing pages | Affiliate policy, monitoring process, sample creatives |

| International sales | Fraud exposure and currency handling | Country mix, currency plan, fraud tools |

| Chargebacks | Ratios, root causes, prevention tools | Chargeback report, refunds, alert tools, RDR status |

Billing Descriptors and Renewal Communication

A confusing descriptor is one of the simplest ways to turn a legitimate renewal into a dispute. The customer may not remember the product, may see a parent company name they do not recognize, or may not know how to contact support.

Cybersecurity merchants should use brand-recognizable descriptors whenever possible. If the processor supports it, adding a customer service phone number can reduce bank disputes by giving the cardholder a direct path to the merchant.

Renewal communication matters just as much. Companies with lower dispute rates often send advance renewal reminders, confirmation emails after renewal, receipts with support contact information, and easy self-service account management links.

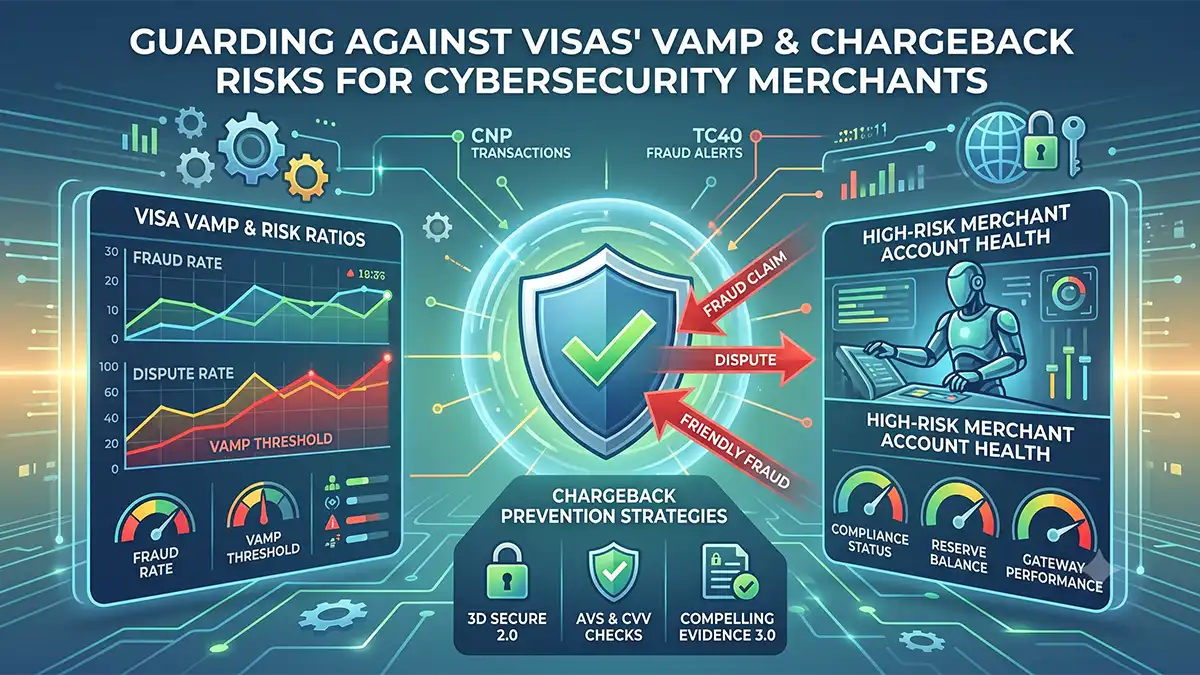

Visa VAMP and Proactive Dispute Management

Visa's Acquirer Monitoring Program, commonly referred to as VAMP, has increased the need for proactive dispute management. Cybersecurity merchants are especially exposed because recurring billing, global customers, digital delivery, and friendly fraud can combine into elevated dispute ratios.

Common VAMP contributors include unrecognized transactions, poor support accessibility, slow refund handling, and missing chargeback deflection programs. When customers cannot reach the merchant quickly, they frequently contact the issuing bank instead.

Tools such as Rapid Dispute Resolution, Consumer Clarity, Order Insight, alert-based dispute prevention, and chargeback alerts can reduce dispute escalation. The goal is to resolve confusion before it becomes a formal chargeback.

Rolling Reserve Reduction Strategies

Rolling reserves are common in higher-risk e-commerce and recurring billing environments, but they are not always permanent or fixed. Underwriters may reduce reserve requirements when a merchant shows stable volume, low chargeback ratios, consistent operations, strong cash flow, and active dispute controls.

Financial strength also matters. Bank statements, financial statements, cash reserves, and evidence of business liquidity help processors evaluate whether the company can absorb refunds, disputes, and temporary volume swings.

The strongest reserve negotiation is built before the application is submitted. A merchant that presents processing history, refund policies, customer support structure, billing disclosures, chargeback controls, and financial documentation gives the underwriting team a reason to approve more favorable terms.

International Processing Options for Cybersecurity Companies

Many cybersecurity companies sell to customers outside the United States. That global demand can increase revenue, but it may also create cross-border authorization declines, currency mismatch, regional fraud triggers, and customer experience issues.

Global customers increasingly expect local currencies, regional payment options, and checkout flows that look familiar. Multi-currency processing can improve authorization rates, customer experience, and conversion rates when implemented with the right acquiring relationships.

Merchants with substantial international volume often benefit from processing relationships designed for global software businesses, rather than a domestic-only setup that treats cross-border activity as an exception.

Chargeback Prevention Best Practices

- Use transparent product descriptions so customers understand what they are buying and how the product is delivered.

- Display accurate billing disclosures at checkout, in terms, in receipts, and in renewal communications.

- Keep support accessible through visible email, phone, chat, ticketing, or account portal options.

- Implement dispute deflection with RDR, Consumer Clarity, Order Insight, chargeback alerts, and alert-based refund workflows.

- Deploy fraud tools such as device fingerprinting, velocity controls, geolocation screening, and risk-based transaction scoring.

- Monitor early warning signals including chargeback ratios, refund activity, complaints, and cancellation trends.

What to Prepare Before Applying

A cybersecurity merchant account application should not be treated as a basic form submission. The stronger approach is to prepare a complete underwriting package that answers the obvious questions before the bank has to ask.

Useful materials include product descriptions, website URLs, checkout screenshots, refund and cancellation policies, customer support details, billing descriptor examples, monthly volume projections, processing history, bank statements, chargeback reports, affiliate policies, and international sales breakdowns.

When those documents are organized, a processor can more easily understand the merchant's actual risk profile. That can improve approval odds, reduce back-and-forth, and support better terms.

MIDsource helps software, SaaS, antivirus, cybersecurity, VPN, and subscription merchants navigate underwriting, reserves, chargeback prevention, gateway setup, and processor placement. The objective is not just approval. It is stable payment processing that can support long-term growth.

Key Takeaways

- Prioritize billing transparency before underwriting or customers raise concerns.

- Use brand-recognizable billing descriptors and visible support contact details.

- Monitor Visa VAMP exposure and dispute ratios before they become processor problems.

- Implement dispute prevention solutions such as RDR, Consumer Clarity, Order Insight, and alerts.

- Maintain strong financial and operational controls to support reserve negotiations.

- Work with banking partners familiar with software, SaaS, cybersecurity, and subscription-based business models.

If your cybersecurity, antivirus, VPN, or SaaS company needs a confidential review of its processing environment, schedule a call with MIDsource or contact the risk team at risk@midsource.io.

Outside Data That Supports the Guide

The outside data below supports the same themes security software merchants face every day: subscription transparency, checkout trust, global payment preferences, and card-network fee structure all affect payment stability.