Rolling reserves are one of the most common pain points for cybersecurity and antivirus merchants. A reserve can protect the processor, but too much reserve pressure can restrict cash flow and slow growth.

Why Reserves Are Required

Processors use reserves when they believe future refunds, chargebacks, or operational changes could create financial exposure. Cybersecurity merchants may face reserves because they bill recurring subscriptions, serve global customers, deliver digital goods, or have prior processing issues.

A reserve does not always mean the business is bad. It means the underwriting team wants a buffer while it evaluates performance over time.

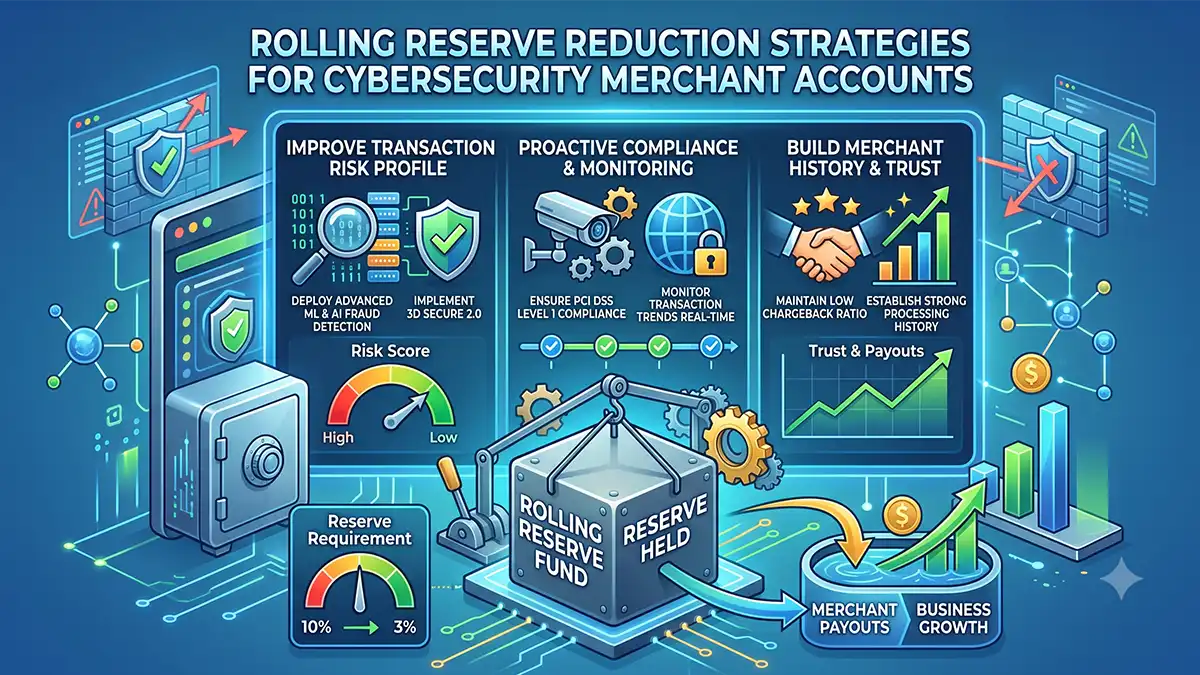

Factors That Can Reduce Reserve Requirements

- Stable processing history: consistent monthly volume, low chargeback ratios, and steady operations improve confidence.

- Strong financials: bank statements, financial statements, cash reserves, and liquidity support lower perceived risk.

- Active dispute management: RDR, Consumer Clarity, Order Insight, alerts, and refund workflows show the merchant is controlling exposure.

- Clear billing practices: renewal reminders, recognizable descriptors, and accessible cancellation reduce friendly fraud.

- Experienced processor placement: banking partners familiar with software and cybersecurity can structure terms more appropriately.

Documentation for Reserve Negotiation

Merchants should prepare recent processing statements, chargeback reports, refund reports, bank statements, financial statements, product descriptions, renewal language, cancellation policy, and support procedures.

If reserve terms are already in place, the merchant should track performance over time and request periodic reviews. A processor is more likely to revisit reserves when the merchant can show improved ratios, stable volume, and strong cash flow.

| Reserve Concern | Processor Question | Merchant Evidence |

|---|---|---|

| Disputes | Will chargebacks rise? | Low ratios, alert tools, refund workflow |

| Cash flow | Can refunds be covered? | Bank statements and liquidity |

| Volume spikes | Can operations support growth? | Volume history and forecast explanation |

| Billing confusion | Will customers recognize charges? | Descriptors, notices, support links |

When to Seek a New Processing Relationship

If reserves keep increasing without a clear review path, or if volume caps prevent legitimate growth, it may be time to evaluate alternate processor placement. The goal is not simply to avoid reserves. The goal is to find terms that match the actual risk profile of the business.

Cybersecurity merchants with strong controls should not be treated the same as poorly documented merchants with unmanaged disputes. Presenting the right evidence can change that conversation.

MIDsource helps software and cybersecurity merchants review reserve terms, prepare underwriting packages, and pursue processor relationships designed for recurring digital businesses. Learn about high risk merchant accounts.

Visual Aid: Reserve Negotiation Scorecard

Rolling reserves are usually reduced when the processor can see repeatable evidence of lower risk. The strongest negotiation file does not argue that the business is low risk; it proves that the risk is measured, controlled, and financially supported.

Data and Source Context

Visa explains that merchants pay a negotiated merchant discount to their financial institution, and that processing services may be included in that rate. For high-risk software merchants, reserves are another form of processor risk management layered onto the account economics. Visa source

The FTC's subscription complaint trend is relevant because hard-to-cancel or confusing recurring billing can increase refund and dispute pressure. More complaint pressure means more evidence underwriters may request before lowering reserves. FTC source