Antivirus and cybersecurity companies often assume a processor decline means the bank does not understand the product. Sometimes that is true. More often, the decline comes from risk signals that were not documented clearly enough during underwriting.

The Specialized Risk Profile

Cybersecurity software is typically sold online, fulfilled digitally, renewed automatically, and marketed to customers in multiple regions. Each of those traits can be legitimate, but together they create a payment profile underwriters review closely.

A processor wants to know whether customers understand the charge, whether refunds are handled quickly, whether support is accessible, whether affiliate claims are controlled, and whether prior chargebacks or terminations suggest future risk.

Five Common Decline Triggers

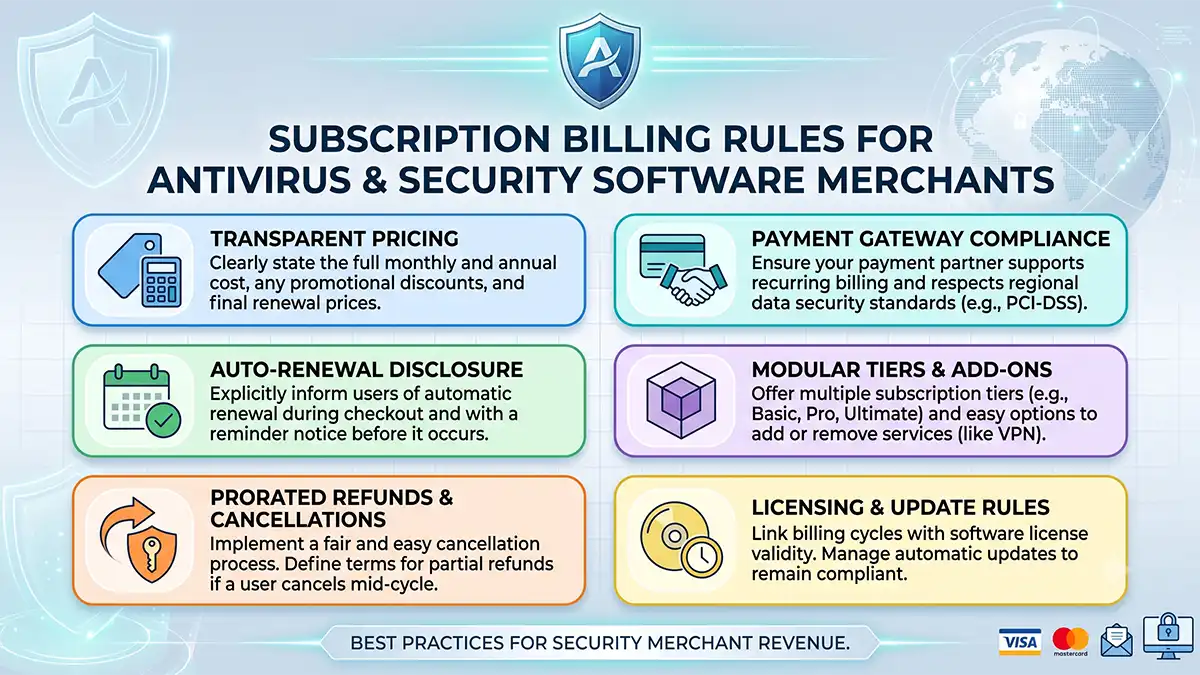

- Recurring billing concerns: automatic renewals, trial-to-paid conversions, and forgotten subscriptions can create disputes if terms are unclear.

- Historical chargeback activity: even moderate dispute levels can lead to application declines, reserve requirements, or reduced volume limits.

- Affiliate marketing exposure: underwriters may review advertising practices, landing page disclosures, and affiliate oversight controls.

- International processing activity: cross-border transactions can trigger fraud concerns, currency mismatch, and geographic risk exposure.

- Prior processor terminations: past reserve increases, volume restrictions, or closures can create additional scrutiny.

Underwriting tip: Do not wait for the processor to ask for proof. Prepare checkout screenshots, renewal language, refund policy, cancellation flow, support details, chargeback reports, and affiliate controls before submission.

How to Improve Approval Odds

The strongest antivirus merchant applications explain the business model in plain language and support it with documentation. Product pages should accurately describe the software, pricing should be visible, renewal terms should be clear, and cancellation should be easy to find.

Merchants should also explain their traffic sources. If affiliates are used, show how affiliates are approved, monitored, and removed when they violate policy. This helps underwriters separate controlled affiliate programs from high-risk lead generation.

Finally, be direct about prior processing history. If a previous processor imposed reserves or limits, explain what changed: new refund procedures, dispute alerts, clearer descriptors, better fraud screening, or lower chargeback ratios.

What MIDsource Reviews

- Business model and fulfillment process

- Website, checkout, terms, privacy, refund, and cancellation pages

- Billing descriptors and customer support visibility

- Monthly volume, average ticket, countries served, and card mix

- Chargeback history, refund activity, and dispute prevention tools

A decline is not always the end of the road. For many cybersecurity merchants, the better move is rebuilding the application around the real risk controls the business already has in place. Talk with MIDsource for a confidential review.

SEO Data: What Underwriters Are Really Trying to Predict

Processor declines usually come from concentration of risk, not one isolated issue. An antivirus merchant with recurring billing, affiliate traffic, international customers, and prior disputes gives the bank multiple reasons to slow down or decline the file.

Decline Risk Signals by Underwriting Priority

Scored as an underwriting-priority index for cybersecurity and antivirus merchant-account risk factors, not as an industry decline-rate claim.

Credible Source Context

Visa's merchant-facing rules page explains that its payment system includes operational requirements designed to keep transactions secure and reliable. For cybersecurity merchants, that means underwriting teams are trying to document whether the account can process predictably, resolve customer issues, and maintain acceptable dispute levels. Visa source

Baymard's checkout research is useful context because it shows how trust and checkout clarity influence customer behavior: 19% of surveyed U.S. online shoppers abandoned a checkout because they did not trust the site with credit card information, and 8% cited a declined credit card. Those same trust and decline issues can show up later as processor concerns for digital software merchants. Baymard source