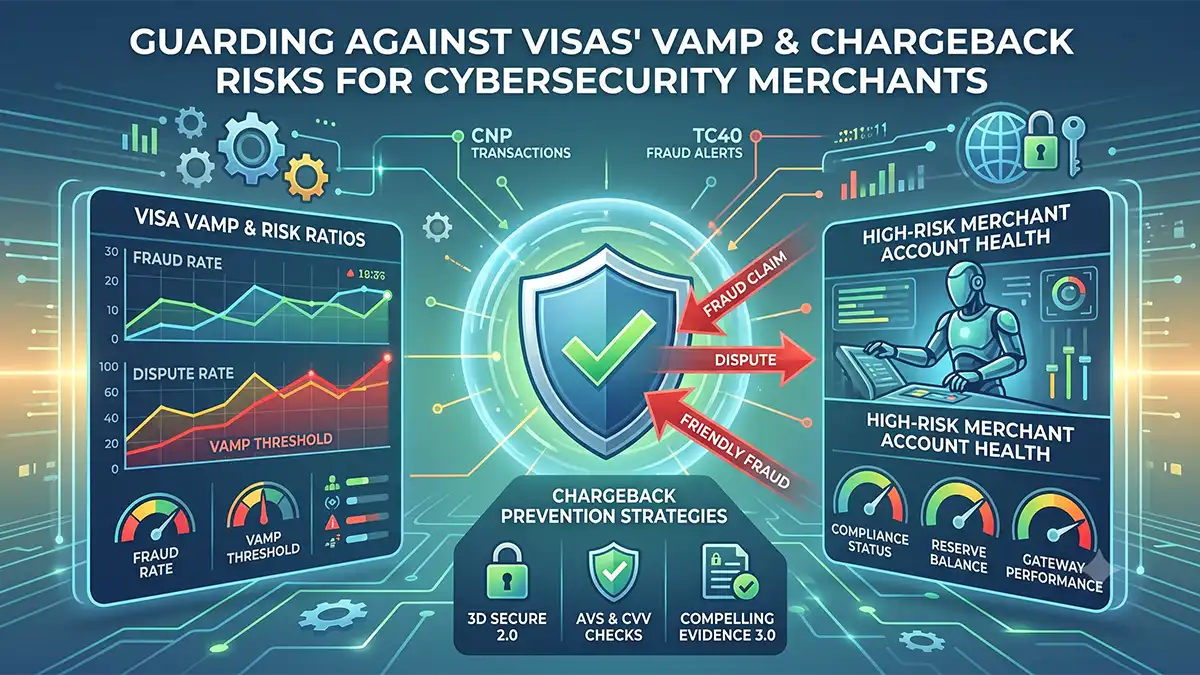

Visa's Acquirer Monitoring Program, known as VAMP, has made dispute ratios harder to ignore. For cybersecurity merchants, the best approach is to prevent confusion before it becomes a chargeback.

Why Cybersecurity Merchants Are Exposed

Antivirus, VPN, endpoint protection, and SaaS security merchants often combine recurring billing, digital delivery, international customers, and friendly fraud exposure. That combination can elevate dispute ratios if customer communication is weak.

A customer may forget a renewal, fail to recognize a descriptor, have trouble reaching support, or assume a bank dispute is the fastest refund path. Each event may feel small on its own, but together they can create processor monitoring pressure.

Common VAMP Contributors

- Unrecognized transactions: customers forget software renewals or do not recognize the billing descriptor.

- Poor support accessibility: customers go to the issuing bank when the merchant is hard to reach.

- Inadequate chargeback deflection: merchants fail to use RDR, Consumer Clarity, Order Insight, alerts, or fast refund workflows.

- Weak renewal communication: customers are not reminded before recurring billing occurs.

- Fraud screening gaps: suspicious behavior is not caught before authorization.

Important: Chargeback prevention is not only about fighting disputes. For recurring software merchants, the bigger win is reducing formal disputes before they affect monitoring ratios and processor relationships.

Dispute Deflection Tools

Rapid Dispute Resolution can automatically resolve certain disputes before they become chargebacks. Consumer Clarity and Order Insight can give issuers more transaction detail, helping cardholders recognize legitimate purchases. Alert services can notify merchants early enough to issue refunds when appropriate.

The right combination depends on the merchant's product, countries served, processor setup, gateway, and dispute history. The important part is having an active program rather than waiting for monthly statements to reveal a problem.

Fraud Prevention Controls

- Device fingerprinting to identify suspicious repeat behavior

- Velocity controls for repeated purchase attempts

- Geolocation screening for unusual country or IP patterns

- Risk-based transaction scoring

- Refund and cancellation trend monitoring

- Customer complaint tracking before disputes escalate

Operational Practices That Help

Make customer service easy to find. Add support links to receipts, renewal notices, account dashboards, and product emails. If a phone number can be included in the billing descriptor, use it.

Track chargeback ratios, refund activity, customer complaints, and subscription cancellation trends weekly or monthly. Early identification gives the merchant time to adjust billing language, support staffing, fraud settings, or refund rules before processor intervention occurs.

MIDsource works with cybersecurity and subscription merchants to review VAMP exposure, chargeback causes, and prevention tools. Explore chargeback prevention services or schedule a confidential review.

Visual Aid: How Disputes Escalate Into Processor Risk

Visa describes its system as a rules-based payment environment built to minimize risk and support secure, reliable global transactions. For cybersecurity merchants, VAMP exposure is usually a symptom of customer confusion, weak support access, missing dispute-deflection tools, or fraud controls that are not tuned to digital recurring billing.

Chargeback Prevention Control Stack

Priority model built from common VAMP contributors and dispute prevention recommendations for recurring cybersecurity merchants.

Source-Backed Context

Visa's public small-business page explains that Visa rules are designed to reduce risk and support a secure global payment experience, while its interchange structure involves acquirers, issuers, and merchant discount rates. This is why a merchant's dispute behavior can affect processor treatment even when the merchant sells legitimate software. Visa source

Baymard's checkout data also supports the trust angle: 19% of U.S. online shoppers in its study cited lack of trust with credit card information as a reason for abandonment. Trust gaps at checkout can become dispute gaps after renewal. Baymard source